Industry

Balanced Scorecard

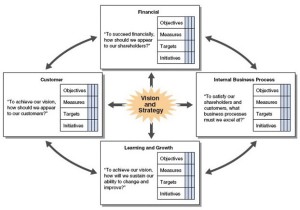

In 1992, Robert S. Kaplan and David Norton introduced the functionality measurement balanced scorecard, a concept for measuring a business’ activities in terms of its vision and techniques, to give managers a complete view of the performance of a business. The essential new element is focusing not only on monetary outcomes but also on the human troubles that drive these outcomes, so that organizations concentrate on the future and act in their long-term ideal interest. The strategic management method forces managers to concentrate on the essential efficiency metrics that drive achievement. It balances a economic perspective with customer, method, and employee perspectives. Measures are usually indicators of future functionality. The balanced scorecard provides executives with a comprehensive framework that translates a company’s vision and method into a coherent set of performance measures.

A Balanced Scorecard is produced up of four elements: mission, perspectives, objectives, and measures. Each of these elements and how they create on each and every other is described below :

# Mission

The mission is the highest, guiding level of the scorecard. It answers the queries:

– What is our all round reason for getting?

– What is our mission?

– Why do we exist as an organization?

# Perspectives

Perspectives represent the different places that influence overall performance and overall achievement of the mission. There are generally 4 to five perspectives inside a scorecard, however there can be a lot more primarily based on the demands of the organization. Perspectives answer the query “What are our key regions of focus in trying to accomplish our mission?” According to (Kaplan and Norton, 1996), the balanced scorecard supplements conventional financial measures with criteria that measure functionality from three added perspectives – these of clients, internal company processes, and finding out and development:

a. Economic Viewpoint

Economic overall performance measures indicate no matter whether a company’s strategy, implementation, and execution are contributing to bottom-line improvement. Economic objectives typically relate to profitability measured, for example: operating income, return on assets, cash flow, financial worth added.

b. Consumer Viewpoint

Managers identify the client and industry segments in which the enterprise will compete and the measures of the company unit’s overall performance in these targeted segments. This point of view usually consist of a number of core or generic measures of the effective outcomes from properly formulated and implemented strategy. The core outcome measures contain: customer satisfaction, buyer retention, buyer acquisition, buyer profitability, and industry and account share in targeted segments.

c. Internal Organization Viewpoint

The internal organization approach point of view, executive determine the vital internal processes in which the organization must excel. This approach allow the company unit to deliver the value propositions that will attract and retain buyers in targeted market place segments and satisfy shareholder expectation of excellent monetary returns.

d. Finding out and Development Perspective

This perspective identifies the infrastructure that the organization have to build to develop lengthy term growth and improvement. The customer and internal company processes perspectives determine the elements most crucial for present and future achievement.

The four perspectives of the scorecard permit a balance in between quick and lengthy term objectives. The balanced scorecard fosters a balance among distinct strategic measures in an effort to obtain aim congruence, therefore encouraging staff to act in the organization’s best interest. It is a tool that aids the company’s concentrate, improves communication, sets organizational objectives, and offers feedback on strategy.

# Objectives

Inside every single point of view, objectives identify what needs to be accomplished in order to attain the all round mission. They answer the queries:

– What have to we do (from every viewpoint) to attain the general mission?

– What is most critical (from each perspective) to achieving the general mission?

# Measures

Measures give a way to establish how an organization is carrying out in attaining the objectives inside the perspectives and in turn the overall mission. They are the most “actionable” element in the scorecard. For every measure, a target is set so that progress toward the objective can be evaluated. Measures answer the question:

“How do we know how well we’re carrying out in reaching our objectives, and in turn our general mission?”